Commentary & Analysis

Available Alternatives to Hormuz for Gulf Oil Exporters

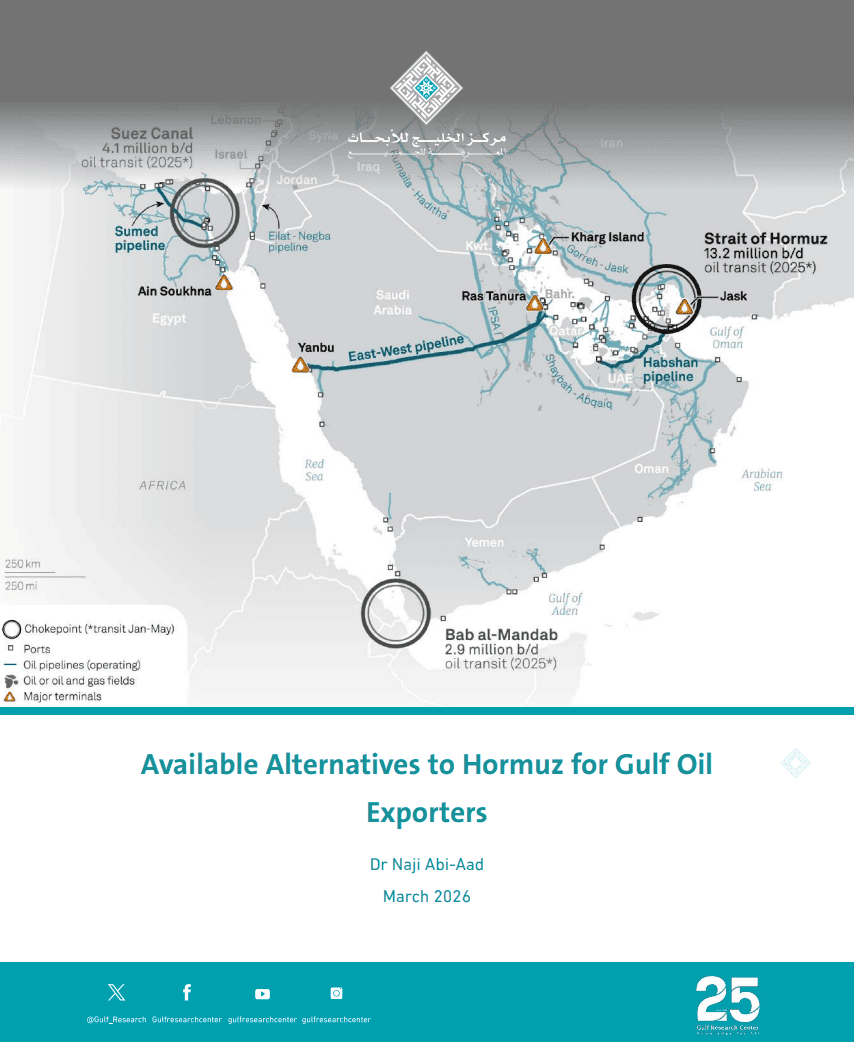

At the beginning of March 2026, the Strait of Hormuz, a vital artery for global oil and gas trade located between Oman and Iran, was de facto closed by Tehran who warned that any vessel attempting to transit the waterway would be targeted. While in 2025 roughly 13 million barrels per day (b/d) of oil passed through Hormuz, representing about 31 percent of all seaborne crude flows, some 85 million tons of liquefied natural gas (LNG), or around 21 percent of the global LNG trade, were channelled through the strait.

While there are no alternative pipelines or shipping routes that could bypass the Strait of Hormuz and handle even a fraction of the missing volumes of LNG from the Gulf, a few oil exporters in the region, notably Saudi Arabia, Iraq, the United Arab Emirates (UAE), and Iran have built many alternate export outlets over the years aimed at bypassing the vulnerable Hormuz. Those oil exporters are now increasing shipments from alternative routes, but the total volumes are far from enough to offset the entire drop from the crisis-hit strait. Other oil producers in the Gulf either have no export outlets outside Hormuz, such as Kuwait and Qatar, or have their loading terminals located on open sea, such as Oman. In fact, the Omani oil loading and export terminals are strategically located outside the Strait of Hormuz, with key facilities on the Gulf of Oman (Ras Markaz) and the Arabian Sea (Mina Al-Fahal and the Port of Duqm).

It is worth mentioning that the alternative export pipelines for Gulf oil remain vulnerable and subject to closure and pumping disturbances, comparable to the fate of many crude pipelines in the region, especially those crossing more than one border. When looking at the historical performance of the oil export pipelines in the Gulf, one could easily note that every line in the region has been shut down at least once, and that most of them remain closed until the present time.

The main reasons behind the shutdown of many export pipelines in the Gulf remain the political conflicts within producing countries or transit states, and interstate disputes. In fact, most of the pipelines crossing state boundaries have fallen victim to the region’s political rivalries and conflicts at one point or another.

On other side, the opening of closed or new pipelines is subject not only to the political will of the concerned countries, but also to the economic realities and requirements of the oil market. Gulf exporters for example may not need to pump so much oil through the Mediterranean terminals considering the saturation of European markets and the need to export much of their crude to Asian outlets, the main prospective oil markets in the coming decades.

Saudi Arabia

In response to the de facto closure of the Strait of Hormuz, Saudi Arabia has increased oil shipments from the Red Sea, by loading up to 77 percent of its total crude exports (around 6.5 million b/d in 2025) at its Yanbu terminal. Yanbu is linked to the oil-producing Eastern Province across the width of the Arabian Peninsula through the 5 millionb/d East-West Pipeline, also known as Petroline. Petroline was built during the 1980-88 Iran-Iraq war to secure outlets other than on the Gulf, and to lessen the Kingdom’s dependence on the vulnerable Strait of Hormuz. At one point, the line was converted to carry natural gas to power plants in the Kingdom’s western provinces, but was then switched back to pump crude oil.

In addition to the East-West pipeline, Saudi Arabia could hypothetically use other alternative export outlets, such as the old Iraqi Pipeline through Saudi Arabia (IPSA) and the Trans-Arabian Pipeline (Tapline).

The 1.65-million b/d IPSA which originally travelled from the Al-Zubair field in southern Iraq through Saudi Arabia to the Red Sea port of Mu’ajiz, just north of Yanbu, was built in 1987 after oil tankers were attacked in the Gulf during the Iran-Iraq war. However the line has not carried Iraqi crude since the Iraqi invasion of Kuwait in August 1990. Riyadh subsequently confiscated IPSA in 2001 as compensation for debts owed by Baghdad.

In the early years of the new decade, the Saudi government used IPSA to transport gas to power plants in its western provinces. However, in 2012 concerns over the potential closure of the Strait of Hormuz led Riyadh to pump test volumes of crude through the pipeline. Then, in 2018 Saudi Arabia announced serious plans to use IPSA and the Mu’ajiz terminal to export its oil through the Red Sea.

Although the Kingdom seldom used IPSA to pump its crude, the pipeline provides more strategic flexibility, acting as a hedge against disruptions around Hormuz by giving Riyadh more scope for exporting its crude from Red Sea terminals in the event that the Strait is blocked. IPSA, together with the East-West pipeline, could very well provide export outlets for around 6.6 million b/d of Saudi crude, which is almost equal to the Kingdom’s oil exports in 2025.

The Trans-Arabian Pipeline (Tapline) could, if and when reopened, hypothetically add more potential for channelling Saudi crude to the Mediterranean Sea. Tapline was built in 1950, spanning from the Saudi Eastern Province to the Zahrani terminal south of the Lebanese town of Sidon on the Mediterranean coast. The 500,000- b/d pipeline was an important factor in the global trade of petroleum, as well as in American-Middle Eastern political relations. Tapline, as well as the Iraqi lines through Syria and Lebanon (see below), were priceless immediately following the closure of the Suez Canal in June 1967. However, with the introduction of supertankers, shipping regained some of its economic advantage.

Tapline was built and operated by the TransArabian Pipeline Company (TAP), now a fullyowned subsidiary of Saudi Aramco. It largely ceased functioning in 1983 as a result of the exorbitant fees on the pipeline’s oil imposed by the transit countries, and Syria in particular, which undermined the line’s economic value, before completely halting operations in 1990. According to sources at Saudi Aramco, the pipeline is still in excellent condition being regularly and amply maintained and cathodically protected, whereas its communication system would require some modernisation updates in order to adapt it to the latest technological developments. In addition, the pumping stations need some rehabilitation work if the pipeline is to pump again at its top nominal capacity, especially since they have been idle for over 35 years.

The Tapline corridor remains a potential direct export route for Saudi oil to Europe and the United States. Transportation costs to export oil via Tapline to Europe would actually cost as much as 40 percent less than shipping by tanker through the Suez Canal.

Iraq

In Iraq, two oil export terminals are operating on the Gulf, southeast of the Al-Faw Peninsula, including the Basrah and Khawr Al-Amiyah terminals. These critical offshore facilities can handle over 80 percent of Iraq’s oil exports, especially those destined for Asian markets.

Nevertheless, Iraq, with its meagre Gulf coastline, has consistently sought the diversification of its export channels. It is now able to export part of its oil through pipelines to the Turkish Mediterranean port of Ceyhan. The first pipeline from the large Kirkuk field to Ceyhan was completed in 1976.

Four years later, the start of the Iran-Iraq war was a stimulating factor for Baghdad to plan and build a second parallel pipeline to Ceyhan, which was added in 1987.

The dual Iraqi pipeline system to Ceyhan with a total nominal capacity of 1.6 million b/d has been providing an alternate route to export Iraqi crude. Potentially, it has the capacity to channel around 48 percent of all Iraqi exports (roughly 3.4 million b/d in 2025). Nevertheless, pumping through this dual pipeline which passes through Kurdish regions has been subsequently interrupted several times due to conflicts, ensuing sanctions, and attacks on multiple fronts.

Thus, Iraq needs to reach an agreement with the autonomous Kurdistan to facilitate oil exports through the pipelines to Ceyhan. In addition, Baghdad should rehabilitate the Strategic Pipeline which links its prolific southern fields with the transportation system in the central and northern parts of the country. This is also a prerequisite if Iraq wants to reopen other export outlets which remain closed for various reasons.

One of those outlets is the old IPC (Iraq Petroleum Company) pipeline from the Kirkuk field to the Mediterranean Syrian terminal of Banias, together with a branch line to the loading facility at the port of Tripoli in northern Lebanon. The Kirkuk-Banias/ Tripoli 700,000-b/d pipeline which was completed in 1952, repeatedly fell (and is still) victim to IraqiSyrian antagonism which resulted in its closure since April 1982. Recent rumours were heard of the possible rehabilitation and re-opening of the pipeline following the 2024 radical change in the Syrian regime, although no concrete steps have been taken in this direction since then.

The UAE

Crude oil in Abu Dhabi, the main oil producing emirate of the UAE, used to be mostly exported through the Oylz terminal at the Khalifa Port, and the oil loading facility at the Mubarraz Island, both within the Gulf, before the construction of the Abu Dhabi Crude Oil Pipeline (ADCOP) in 2012.

The 1.5 million-b/d ADCOP pipeline from the Habshan onshore field in Abu Dhabi which travels overland and then across the barren Hajar Mountains to the emirate of Fujairah on the Gulf of Oman, was commissioned by the International Petroleum Investment Company (IPIC) of Abu Dhabi in order “to increase the security of supply and reduce the transportation of Emirati oil through the Strait of Hormuz.” ADCOP is actually allowing Abu Dhabi to bypass Hormuz and channel around 55 percent of its exports (estimated at about 2.7 million b/d in 2025) from the Fujairah terminal.

Iran

The primary export hub for Iranian oil has been the Kharg Island which handles up to 90 percent of the country’s crude exports. In addition, Tehran relies on oil export facilities at the islands of Sirri and Lavan, as well as Ras Bahregan and Bandar Abbas.

Those Iranian oil export facilities are located within the Gulf, and this fact led the government in Tehran to develop in 2021 a strategic oil export terminal at Jask on the Gulf of Oman, which is supported by a 1,000-km crude pipeline from the Goureh oil facility. The Jask terminal, with a daily loading capacity of one-million barrels, not only aims to bypass the Strait of Hormuz, but to mainly reduce the country’s heavy reliance on the oil export facilities at Kharg Island.

Final Word

The major crisis in the Gulf since late February 2026 with the start of military conflict between Iran on one hand and the US and Israel on the other, clearly shows the need for oil producers in the region to maintain emergency measures that can be quickly executed if and when their exports through the Strait of Hormuz are blocked for any reason.

In fact, Gulf oil producers should develop and expand alternative outlets to Hormuz for their exports that are capable of being securely and quickly activated, while providing sufficient sustainable capacity to accomodate significant export volumes. Such massive efforts should be pursued at both national and regional levels, with an important coordinating role potentially played by the Gulf Cooperation Council (GCC) for the sake of all its member states, or by other regional bodies that involve all the countries in the region.

Dr . Naji Abi-Aad is the Senior Advisor on Energy Studies at the Gulf Research Center (GRC).